Once, we were looking at whether banks made money on demand drafts (DDs).

DDs are costly. 90% of a bank’s costs are people-related, and it takes a fair bit of time (hence people) to process DDs. If you pay for DDs in cash, it costs even more because the teller has to count the notes.

To recover this cost, banks charge a fee. The fee increases with the size of the DD. A DD for Rs 10,000 may cost Rs 50, while one for Rs 100,000 may cost Rs 200.

But apart from the fee, banks also earn float on the DD. Let’s say you go to a bank, pay Rs 100,000, and take a DD. You mail the DD to someone, who cashes the DD three days later. The bank has your Rs 100,000 for 3 days, and earns the overnight interest rate at around 5%, netting Rs 41 in the process. This float is significant for large DDs.

Our client bank was making a small loss on DDs. Every DD less than Rs 50,000 caused a loss (even after including float). And 3 out of every DDs was smaller than Rs 50,000.

Then we had this bright idea: let’s lower fee for large DDs, attract of them, and get more float income. DDs above Rs 50,000 are profitable. So big DDs are worth going after. 80% of the float income comes from the top 22% of DDs. So surely, the big DDs are worth going after. Float income increases forever, whereas fee income is capped. So big DDs could absolutely be terrific.

We were thrilled. Here was a revolutionary counter-intuitive idea: have lower charges for DDs to get more money. We kept talking about it to our client. But at the end, we didn’t suggest it. It got left behind the conventional idea of increasing the fee for small DDs.

We were a bit disappointed, and kept cursing the conservatism of public sector banks. Goes to show how the bright young consultants can be naive. For, as it later turned out, the bulk of DD revenues is really fee income (88%), not float income. Had we lowered the fee income, there’s would’ve been no chance for the float income to make up for it.

Why did we miss that? A couple of reasons. The simple one was, though the float income increases forever, doesn’t beat fee income until the DD is about Rs 2 crores. DDs typically stay with you for a few days, and you can’t earn much interest on that.

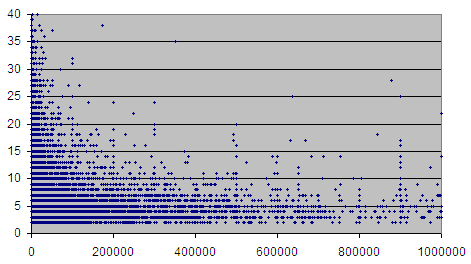

The other reason was subtler. We had assumed that the float income for a DD of Rs 100,000 is 100 times that of the DD income for Rs 1,000. But the float income does not increase linearly! Someone who gets a DD for Rs 1,000 doesn’t mind waiting a bit to present it, but someone who gets a DD for a lakh would walk to the bank the very same day. The chart below shows how long customers wait to cash DDs. The X-axis is the size of the DD. The Y-axis is the number of days they wait. It shows a clear diminishing trend.

Lesson: Conservative bankers might make more money not listening to hotshot consultants.

Comments